Colorado Leads the Region in Venture Capital, But the Data Reveals a Deeper Story

The findings, drawn from venture capital data spanning from 2020 through 2025, reveal a Colorado market that leads on total capital by a wide margin while also exposing a structural challenge that the region cannot afford to ignore.

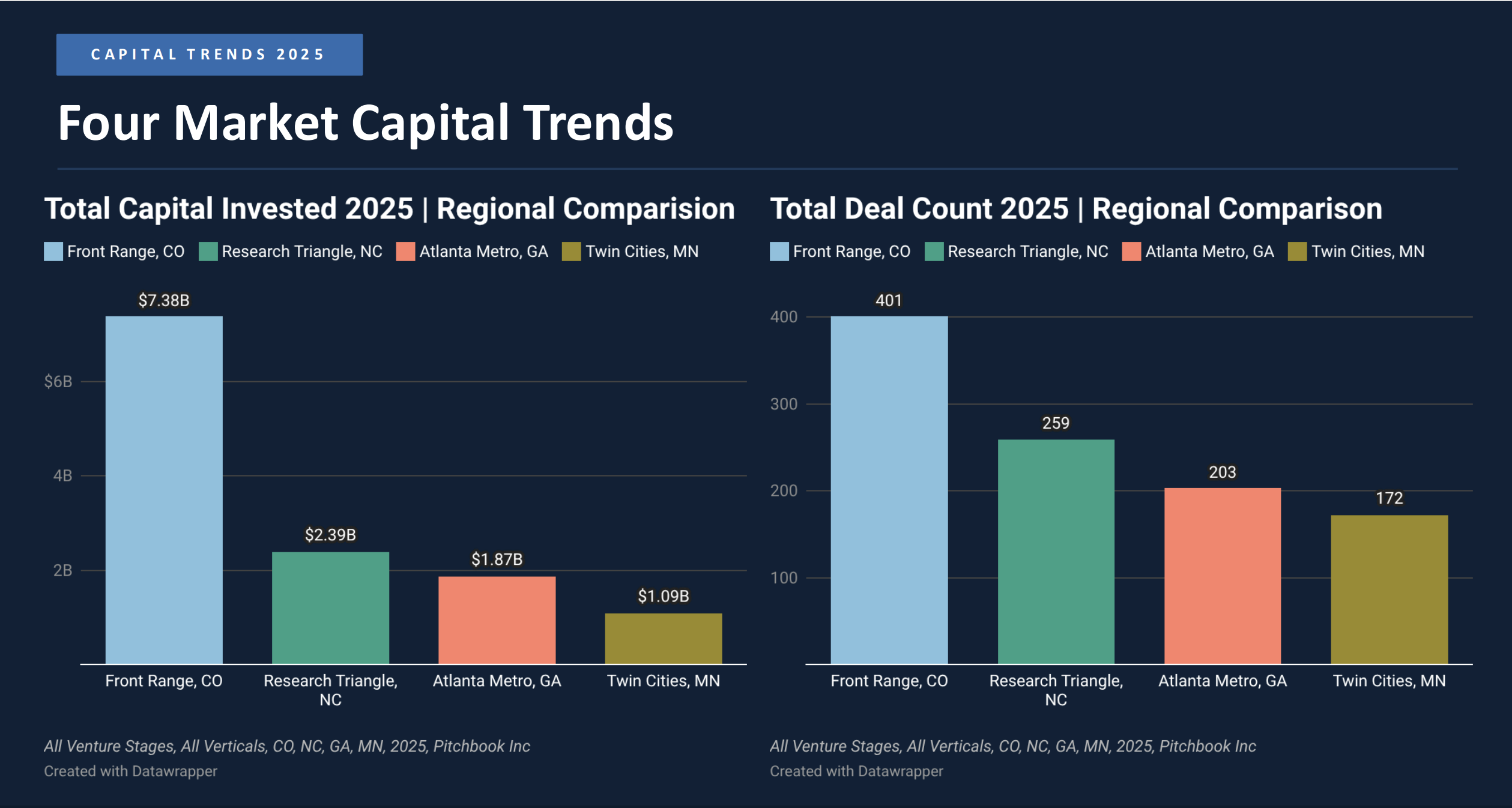

A new report from Innosphere benchmarks the Colorado Front Range venture capital ecosystem against three peer innovation regions: the Research Triangle in North Carolina, the Twin Cities in Minnesota, and the Atlanta Metro in Georgia. The findings, drawn from venture capital data spanning from 2020 through 2025, reveal a Colorado market that leads on total capital by a wide margin while also exposing a structural challenge that the region cannot afford to ignore.

The Current Status of Venture Capital

In 2025, investors deployed nearly $7.4 billion in venture capital across the Colorado Front Range, representing 401 deals and roughly $2,480 in capital per capita. That total exceeded the other three markets combined. By comparison, the Research Triangle attracted $2.4 billion, Atlanta recorded $1.9 billion, and the Twin Cities drew $1.1 billion. Colorado's lead is not marginal. It reflects a genuine concentration of investable companies, research infrastructure, and technology talent that few interior U.S. markets can match.

The sector composition of that capital is worth taking a closer look at. Life sciences attracted the largest share at 36%, followed by energy technology at 26%, and quantum at 15%. These proportions align directly with the work of Innosphere and the NSF ASCEND Engine supporting innovation focus areas including advanced sensing, quantum technologies, space systems, life sciences, and climatetech Between 2021 and 2025, Colorado attracted $2.1 billion in life sciences investment across 385 deals, $3.4 billion in space technology across 112 deals, and $2 billion in energy innovation across 210 deals. Together these industries serve as the anchoring sectors of a regionally distinctive innovation economy.

Structural Factors

And yet, the headline number masks a structural imbalance that the report addresses directly. Of the $7.4 billion deployed in Colorado in 2025, approximately 75% went to later-stage rounds. Angel investment, seed rounds, and early-stage venture capital together accounted for roughly $2.3 billion. That ratio reflects a market where capital is flowing to companies that have already cleared the hardest early hurdles, as opposed to the ones still trying to get off the ground.

Oftentimes that gap is the space between federally funded research and institutional investment where promising companies most often stall. Innosphere's fund development work, including the launch of a third fund targeting $100 million across America's Innovation Interior, is designed to address exactly that gap. The goal is not to compete with later-stage capital but to ensure that Colorado-grown companies reach the stage where later-stage capital can find them.

All four geographic regions in the study are recovering from the investment contraction that followed the Federal Reserve's rate-hiking cycle in 2022 and 2023. Deal counts are down from 2021 highs across the board, but median deal sizes are rising, reflecting a market that is concentrating capital into higher-conviction bets. Colorado, with a median deal size of $2.5 million in 2025, is recovering faster than its peers. The window to build early-stage infrastructure that captures the next generation of growth companies is open now. The report makes a persuasive case that Colorado needs to use it.

The full Regional Venture Capital Comparison Report is available on the Innosphere website and at this link.